Mario Draghi, President of the ECB: Statement to the press conference (with Q&A)

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2014-07-04 08:42

Introductory statement to the press conference (with Q&A)

Mario Draghi, President of the ECB,

Frankfurt am Main, 3 July 2014

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. The latest information signals that the euro area economy continued its moderate recovery in the second quarter, with low rates of inflation and subdued monetary and credit growth. At the same time, inflation expectations for the euro area over the medium to long term continue to be firmly anchored in line with our aim of maintaining inflation rates below, but close to, 2%.

The combination of monetary policy measures decided last month has already led to a further easing of the monetary policy stance. The monetary operations to take place over the coming months will add to this accommodation and will support bank lending. As our measures work their way through to the economy, they will contribute to a return of inflation rates to levels closer to 2%.

Concerning our forward guidance, the key ECB interest rates will remain at present levels for an extended period of time in view of the current outlook for inflation. Moreover, the Governing Council is unanimous in its commitment to also using unconventional instruments within its mandate, should it become necessary to further address risks of too prolonged a period of low inflation. We are strongly determined to safeguard the firm anchoring of inflation expectations over the medium to long term.

As a follow-up to the decisions taken in early June, the Governing Council today also decided on specific modalities for the targeted longer-term refinancing operations (TLTROs). The aim of the TLTROs is to enhance the functioning of the monetary policy transmission mechanism by supporting lending to the real economy. A press release on the modalities for the TLTROs will be published today at 3.30 p.m. As announced last month, we have also started to intensify preparatory work related to outright purchases in the ABS market to enhance the functioning of the monetary policy transmission mechanism.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP in the euro area rose by 0.2%, quarter on quarter, in the first quarter of this year. Economic indicators, including survey results available up to June, signal a continuation of the very gradual recovery in the second quarter of 2014. Looking ahead, domestic demand should be supported by a number of factors, including the further accommodation in the monetary policy stance and the ongoing improvements in financing conditions. In addition, the progress made in fiscal consolidation and structural reforms, as well as gains in real disposable income, should make a positive contribution to economic growth. Furthermore, demand for exports should benefit from the ongoing global recovery. However, although labour markets have shown some further signs of improvement, unemployment remains high in the euro area and, overall, unutilised capacity continues to be sizeable. Moreover, the annual rate of change of MFI loans to the private sector remained negative in May and the necessary balance sheet adjustments in the public and private sectors are likely to continue to dampen the pace of the economic recovery.

The risks surrounding the economic outlook for the euro area remain on the downside. In particular, geopolitical risks, as well as developments in emerging market economies and global financial markets, may have the potential to affect economic conditions negatively, including through effects on energy prices and global demand for euro area products. A further downside risk relates to insufficient structural reforms in euro area countries, as well as weaker than expected domestic demand.

According to Eurostat’s flash estimate, euro area annual HICP inflation was 0.5% in June 2014, unchanged from May. Among the main components, services price inflation increased from 1.1% in May to 1.3% in June, while food price inflation fell from 0.1% to -0.2%. On the basis of current information, annual HICP inflation is expected to remain at low levels over the coming months, before increasing gradually during 2015 and 2016. Meanwhile, inflation expectations for the euro area over the medium to long term continue to be firmly anchored in line with our aim of maintaining inflation rates below, but close to, 2%.

The Governing Council sees both upside and downside risks to the outlook for price developments as limited and broadly balanced over the medium term. In this context, we will closely monitor the possible repercussions of geopolitical risks and exchange rate developments.

Turning to the monetary analysis, data for May 2014 continue to point to subdued underlying growth in broad money (M3). Annual growth in M3 was 1.0% in May, compared with 0.7% in April. The growth of the narrow monetary aggregate M1 moderated to 5.0 % in May, after 5.2% in April. The increase in the MFI net external asset position, reflecting in part the continued interest of international investors in euro area assets, has recently been an important factor supporting annual M3 growth.

The annual rate of change of loans to non-financial corporations (adjusted for loan sales and securitisation) was -2.5% in May 2014, compared with -2.8% in April. Lending to non-financial corporations continues to be weak, reflecting the lagged relationship with the business cycle, credit risk, credit supply factors and the ongoing adjustment of financial and non-financial sector balance sheets. The annual growth rate of loans to households (adjusted for loan sales and securitisation) was 0.5% in May 2014, broadly unchanged since the beginning of 2013.

Against the background of weak credit growth, the ongoing comprehensive assessment of banks’ balance sheets is of key importance. Banks should take full advantage of this exercise to improve their capital and solvency position, thereby supporting the scope for credit expansion during the next stages of the recovery.

To sum up, the economic analysis indicates that the current low level of inflation should be followed by a gradual upward movement in HICP inflation rates towards levels closer to 2%. A cross-check with the signals from the monetary analysis confirms this picture.

As regards fiscal policies, substantial fiscal consolidation in recent years has contributed to reducing budgetary imbalances. Important structural reforms have increased competitiveness and the adjustment capacity of countries’ labour and product markets. However, significant challenges remain. To strengthen the foundations for sustainable growth and sound public finances, euro area countries should not unravel the progress made with fiscal consolidation, in line with the Stability and Growth Pact, and should proceed with structural reforms in the coming years. Fiscal consolidation should be designed in a growth-friendly manner, and structural reforms should focus on fostering private investment and job creation. A full and consistent implementation of the euro area’s existing fiscal and macroeconomic surveillance framework is key to bringing down high public debt ratios, to raising potential growth and to increasing the euro area’s resilience to shocks.

Finally, I wish to inform you that the Governing Council today announces that the frequency of our monetary policy meetings will change to a six-week cycle, from January 2015. The reserve maintenance periods will be extended to six weeks to match the new schedule. Moreover, we announce our commitment to publish regular accounts of the monetary policy meetings, which is intended to start with the January 2015 meeting. A press release providing more details will be published today at 3.30 p.m.

We are now at your disposal for questions.

* * *

Question: You said earlier that you decided on some details for the TLTROs. Would you be so kind as to fill us in what these are? And my second question is concerning the forward guidance. You said a couple of weeks ago that interest rates would remain low for a longer period, and you referred to the extension of the full allotment until 2016, as well as to the four-year loans. What exactly do you mean? Thank you.

Draghi: Really, I don't think I ever made an explicit link between the extension of the fixed-rate full allotment or the four years' maturity for the lending and the period of time during which interest rates would remain at the present levels. I always said that the interest rates would remain at present levels for an extended period of time. The length of this period of time depends on our medium-term outlook for inflation. That's the only reference that we should keep in mind.

On the TLTRO, actually, first of all, we mentioned the figure last time of 7% of the loan book of banks amounting approximately to €400billion, and the overall take-up could reach a maximum of €1 trillion, so that is what's available for the banks. Then, it's going to be up to them to make use of this opportunity, which indeed from a financing viewpoint looks attractive.

Now, using our internal analysis, our internal models, we have asked the question whether this new measure, depending on its take-up, will have an impact on the inflation rate and the growth rate of the euro area. And the answer the models gave is that they do have an impact. It's going to be a significant impact, and it will certainly be very helpful. Of course, depending on the take-up, it will be very helpful in taking the inflation rate back to below but close to 2% over the horizon that we have discussed on other occasions.

As far as the details of the TLTROs, let me say just a few things, and then for further questions, I will ask you to read the press statement, and also there will be a debriefing after the press conference by the staff of the ECB on all further questions you may ask.

So let me just go through some of the main elements of the TLTRO. First of all, participation. Banks can either participate individually, or they may form a group if certain criteria are met.

Second, I said this already, the counterparties will be entitled to an initial borrowing allowance equal to 7% of the total amount of their loans to the euro area nonfinancial private sector, excluding loans to households for house purchase outstanding, on April 30, 2014.

Funds up to the initial allowance can be borrowed in two operations, which will be allotted on September 18th and December 11th, 2014. Then, there is an additional allowance, whereby banks can draw additional allowances under the programme if they generate eligible lending over the first two years of the programme in excess of a given benchmark.

The additional allowance amounts to three times the difference between their actual eligible lending and their benchmark. The additional allowance can be borrowed in six TLTRO operations, running from March 2015 to June 2016, so there are six TLTROs at quarterly intervals in this period of time.

The benchmark, now, there will be two types of benchmarks, one for banks that are currently expanding their loan portfolio, so they are positive net lenders, and one for banks that have decreased their lending to the real economy. Namely, they are negative net lenders -- that is to say banks that have been deleveraging in the last 12 months.

By devising these two benchmarks, we took into account that, for some banks, deleveraging is necessary. We certainly don't want to discourage that. It's part of the adjustment process towards a more sustainable finance structure.

The reference period for benchmarks, for both benchmarks, is the 12-month window up to April 30, 2014. The benchmark for positive net lenders, as I said, is the level of eligible loans outstanding on April 30, 2014. Further details will be given to you in the briefing, but basically, you have two types of banks. In one case, the benchmark is their current level of lending. And the second one is the declining trend, as calculated in the 12 months up to April 2014, and the benchmark will be with respect to this declining trend.

However, let me tell you, this declining trend will be a broken trend in the sense that, after one year, the benchmark, which is declining, will become horizontal, so the two banks will be treated the same way after one year, and this is done, in a sense, also to minimise potential distortions. If this sounds a little complicated, I think you're right, and you will certainly get more from the briefing later on.

But I'm confident that the banks will quickly understand that, even though it's complicated, it's also quite attractive.

Question: Mr Draghi, you also reminded us that you intensified your work on the ABS programme or the potential programme. Has that effort yielded any results, and could you update us on those?

And the second question is, if you are going reduce your meetings to every six weeks, can you let us know how you are planning to sync this with the US Federal Reserve? Are you planning to speak before or decide before or after your colleagues in the US?

Draghi: No, we have no plan to synchronise our meetings with anybody else, really, so we'll have our new cycle, and we're not going to think about other monetary policy jurisdictions on this.

On the first point, on the first question, first of all, what's the purpose of this programme? The purpose of this programme is to address the impairment in the bank lending channel, to address fragmentation, which translates itself into different funding access conditions and different risk premiums across the euro areas, countries, members.

There are many aspects of the work that are currently being addressed. They are analysis, legal, accounting and operational. There are several bodies that have been involved, in fact, already for quite some time in this work, which is in fact the revisitation of the overall segment, market segment, of securitisations. And they are the FSB and then the Basel Committee and IOSCO and then the European Commission.

Incidentally, the Basel Committee and IOSCO have produced an announcement today about a broad study on this issue. What sort of ABS is the ECB interested, I would say, in promoting?

I think I've said that last time -- they should be real ABS -- namely, we are interested in ABS, as I said, to heal the impairment of the bank lending channel. And we are interested because we want to channel lending to the real economy, and more specifically, to the SMEs. So it should be real ABS. As I said, no CDO squared or financial derivatives or things like that in this concept.

It should be simple. Simple, as it was securitisation in Europe until a few years, a couple of years before the crisis. And, actually, the most complex structures were certainly not generated in Europe. Banks and other European investors invested into these structures, but they were not, by and large, originated here.

And it should be transparent. One of the reasons why securitisation actually got, rightly so, a bad name was that some of these products were so complicated that they could not be priced correctly, and so that's why transparency is going to be a key feature of this new concept.

Now, we are not starting from zero. The key thing is to be able to have information about the content of these ABSs, and there, two initiatives already existing in the euro area would be extremely helpful. One is the loan level data that the ECB and the ESCB have, so that we have information about the single individual loans. And the second is the credit registers that exist in most euro-area countries.

So the ECB is working on this, and the relevant committees have been working on this to define eligibility, pricing, governance, and they have been working on this now for some time. There is one thing that I read often and it is the following – why are you confident that you actually can give some significant size to this market when there is no market for ABS?

Now, that's not true. As you've seen probably from the paper that we published together with the Bank of England, the outstanding amount of securitisations in the European Union at the end of 2013 was about €1.4 trillion, which is one-fifth of what's in the US. But in the US -- and it's mostly in the US, the market is guaranteed by the government, because you have the securitisation related to real estate and housing mortgages.

In this case, there would be also the interest in promoting securitisation that could actually help, as I said before, lending to the real economy and to the SMEs. So to some extent, the size of the market is endogenous, and it depends very much on certain conditions, one of which is regulation. The regulation after the crises treated, I would say, good ABSs and complex or bad ABSs the same way, and they treated the ABS more severely or differently with respect to assets that are very, very similar, both from a capital viewpoint, capital charges viewpoint, and from the liquidity charges viewpoint.

So this is quite an interesting and potentially important development. This could help banks from two perspectives. One is the funding, and the other one is the capital relief that can be obtained through this channel. Of course, if interest rates stay so low, the funding aspect will become less interesting, because banks can access funding at very low rates from central banks or even their own interbank markets.

On the capital relief, it very much will depend on the regulatory treatment and also on the risk retention, because we certainly want the intermediaries to retain some risk, because we learned painfully, I would say, from the crisis, how, all in all inadvisable it is not to have any risk retention by the intermediaries. I think I stop here. I'm sorry, I was a little too long on this.

Question: You noted that the change in the schedule of the meetings would be accompanied with the publication of minutes or accounts. Would it be possible to have a little bit more information on what sort of form those accounts will take and how you think they're going to help your communication strategy?

And second issue, the Bank for International Settlements said over the weekend that central banks should tighten monetary policy sooner rather than later because they were contributing to what they referred as euphoric financial markets that were out of sync with developments in the real economy. Would it be possible to get your take on the BIS annual report, as well, please?

Draghi: On the first, it would be too early. The Governing Council and the Executive Board of the ECB will be working on different what we call dry runs of these accounts, where we have to decide about lots of things, one of which is what we discussed on other occasions -- namely, if the votes should be with names or not, what sort of proposal is being made to the Governing Council. There are actually quite many aspects in order for the accounts to be a useful source of information.

So we'll be working on that, and as a concept will be shaping out, I will certainly keep you informed. That's one.

On the other point, This is actually quite important. We discussed this report last weekend in Basel, and I would say the following, which probably is not going to surprise you, because it's very much the same that other monetary policymakers in other jurisdictions have stated. We think that our monetary policy is perfectly adequate with respect to our stance. We have a mandate, which is price stability, and the current stance of our monetary policy is geared to achieve this mandate.

However, we are at the same time quite sensitive to the formation, creation, to the presence, of potential financial stability risks. And there, we've taken a number of initiatives to address these risks, from the asset quality review to the stress test to the recapitalisation of banks that are taking place now, as we speak, ahead of the results of the AQR.

Even in our TLTROs operations, if you are careful, you see that we've excluded lending to real estate, for real estate purposes, and to sovereigns. We've introduced this treatment with prudential filters for sovereigns that is quite conservative in our comprehensive assessment. And I think I can go on for a while on these measures that we've taken.

So we are addressing these risks as we see them, but the bottom line of this is that the first line of defence against financial stability risk should be the macro-prudential exercise, macro-prudential tools. I don't think that people would agree with the raising of interest rates now for the ECB. It would be quite an interesting proposition but is one that I wouldn't share.

In fact, as I said, interest rates will stay low for an extended period of time, and the Governing Council is unanimous in its commitment to use also nonstandard, unconventional measures to cope with the risk of a too-prolonged period of time of low inflation. Thank you.

Question: Are there some provisions in the way they are structured that wouldn't allow banks to take the money for two years, use it, for example, to buy government bonds and then repay it back to the ECB?

And as a second question, on rates, you said last month that you had reached the lower bound, but there could be some technical adjustments still. Could you elaborate a bit on that?

Draghi: There certainly are provisions to this extent. If the bank doesn't give evidence that they have produced some net lending with respect to the benchmark, they have to pay it back. And you will get more about the exact features of this payback clause in the briefing post-press conference, but certainly that was a concern of the Governing Council, and we have addressed it with a variety of means.

On the second point, yes, that's what I said exactly, that the interest rates will stay at the present levels. Could I exclude any technical adjustment in interest rates? Certainly not. We will still have that. You see, one good thing about the negative deposit rate is that it helps to keep the corridor size unchanged. It has avoided the narrowing of the corridor, which would be counterproductive for the functioning of money markets in the short term. So that's the answer.

Question: Over the past weeks or months, you've alluded several times to the exchange rate as a fairly important factor for inflation being lower, what was expected. Since you've started making these comments and after the measures in June, the exchange actually has not fallen very much. It may have increased. Do you envisage taking any further measure to try and weaken the exchange rate, or are you happy with current levels?

And the other question is about -- again, about the lengthening of the interval between Governing Council meetings to six weeks. Is that because you feel you don't need to be meeting so frequently, that your work is largely done now and you will not have to intervene so frequently as you've done at the height of the crisis? Or what is the reason for that?

Draghi: Yes. Well, let me answer first the second question. The current situation is and has been for the last two, three years, way more complex than it used to be a few years ago. And the right expectation of markets, of countries, people, public opinion, is that we act to cope with this greater complexity.

Now, this expectation in monthly meetings would be reproduced each and every month. The ECB cannot and should not act every month, and while I'm saying this, we certainly don't think that our job is finished. Not at all. I can restate: the Governing Council is unanimous in its commitment to use also unconventional measures, after the Governing Council just reiterated its commitment to keep the interest rates at the present levels for an extended period of time.

So our job is not finished. The issue is whether we should actually have each and every month the expectation for action. Keep in mind that the expectation for action itself injects a certain market behaviour, produces a certain market behaviour which may have nothing or very little to do with fundamentals. So it could become a self-fulfilling expectation with consequences on the markets.

Our assessment on inflation, as you know, is medium to long term, so our outlook is medium to long term. Our monetary policy measures are not taken on the basis of short-term considerations, from this viewpoint, the Governing Council has decided that a monthly frequency was simply just too tight in this situation, and that's the main reason.

There is also another reason, which is more I would say logistical, and it is that if one wants to have a published accounts of the meetings, it gets a little complicated to have an account if you have monthly meetings. It's easier to have it if you have every six weeks, because it gives space for producing the account in a way that doesn't disturb the expectations for further action and doesn't in a sense confuse the reception by the markets of the previous action that's been taken.

So you have to have an interval of time that is such that the published account doesn't actually create confusion with respect to the decisions that have been taken and doesn't create confusion in the expectations about the decisions that will or might be taken in the future.

Now, the other point was about the exchange rate. I will restate here, the exchange rate is not a policy target. It has become important – not any longer increasingly important – it's definitely very important for our outlook of price stability. We perhaps discussed this on other occasions. When you look at reasons for low inflation today and you compare it with, say, three years ago, you have two stages. In the first stage, for about a year, year and a half, it was mostly the oil price, in general, energy prices, and food prices that contributed for two-thirds to the fall of inflation rate from what it was there, then, and it is today. But then, after one year and a half, it was the exchange rate, because the contribution of energy decreased gradually, and it was the exchange rate. So, of course, the two things can't be added, because the contribution of the exchange rate also works through the oil price and energy prices. But, certainly so, it's very important, and we certainly look at this with great attention.

Question: Regarding regulation, we had in the US BNP found guilty and it was sentenced to a very high fine of almost $9billion, far above the provisions of $1billion in their books. So my question with regards to the AQR in progress is does this means that more attention will be paid to the legal risk that several banks here in your area have to bear, especially when there is an interaction with US authorities?

And second question, more generally to AQR and the stress test to follow, there are some criticisms coming from banks, and more surprisingly from the German regulator this week, saying that seriousness has a priority and not the timing, and the reputation of the process could be at stake. What do you say to these criticisms?

Draghi: With respect to the first question, you understand my reluctance to get into the actual intricacies of the case, but from our viewpoint, the viewpoint of a central bank, of a supervisor, the key thing is that the system is resilient to these risks. So, certainly, attention will be devoted to adequate provisioning for these legal risks. By the way, there is already provisioning for legal risks, so the issue to see whether they're adequate, and also, certainly, there will be attention to where these banks actually carry out their activities.

On the second issue, let me say, first of all, that things are actually going well with the single supervisory mechanism. I was told that there was a meeting by the task force, the comprehensive assessment with banks yesterday, and it was completely uncontroversial.

Let me say also that we are enormously grateful to the national supervisors, without the work of which this effort could not be undertaken. I think this should be understood by all. The work is proceeding as scheduled, so the assessment is positive about what's happened.

But one has to understand that this is a very big and complex effort, because what they have tried to do is to establish a common supra-national supervisory standard that would produce a level playing field for all. So, therefore, it's both different from national practices, and it's distant from the interests of the single countries.

So, on occasion, there may be disagreements, but all in all, the trend of this effort has to be judged positively. Things are going well, and some disagreements have to be discounted, because the effort is certainly complex, but it's worthwhile, I would add. It's really worth doing it.

Question: You repeated that you pay great attention to the exchange rate now, and as part of the measures you took a month ago, the euro hasn't lost against the dollar, obviously. Obviously, investors pay much more attention to the statements and measures by the Federal Reserve. To what extent does that worry you that the ECB is still very much in the shadow of the Federal Reserve?

And the second question, you said that you repeated the danger of a self-fulfilling prophecy due to the expectations of the financial market for the monthly meetings of the ECB Council. To what extent did you personally feel under pressure to take measures by these expectations, expectations that you created yourself?

Draghi: No, it's not a matter of pressure. I will respond to this. It's not a matter of personal pressure or even collective pressure. It's just the fact that the expectations by themselves to be discussed and coped with at very tight frequency do generate market reactions that often have no relation with fundamentals, and that's the key thing. It's not so much a matter of pressure, because, as you've seen, we act when it's needed.

The other thing is about being in the shadow of the Fed. Well, if you look at the behaviour of interest rates in the euro area since I first hinted that we would act, which is what, the beginning of May? And then when I announced the measures in early June, you would see that, in fact, there isn't much relationship between what happens here and what happens there.

Eonia rates went down by 12 basis points to 0.03%. The three-months Euribor went down by 10 basis points, and the one-year OIS went down by 23 basis points. So it shows a fairly -- so far, at least, the euro area has been capable of having a certain amount of difference between -- or producing a certain amount of difference between the monetary policy and the consequence of monetary policy in the euro area as opposed to the United States.

The exchange rate is a different issue. There, to some extent, there are many factors that influence the exchange rate, and I don't want to dwell on each one of them. Certainly, the weakness of the European economy, the very low rate of inflation, the extremely low levels of interest rates, do have an effect on the exchange rate, which isn't -- if you look at the four months ago, it was higher, way higher than it is today. But it's a problem. It is, indeed, because as I say, it affects our objective of price stability.

Question: You mentioned a few times this unanimity to take nonstandard measures if needed. You've said your work isn't finished. If needed, you'll do more. Having had a month to gauge the effects of what you did in June, letting it sink in, do you think that it's less necessary to consider nonconventional measures now than it was a month ago?

And my second question, in terms of the sequencing of any additional moves, do you need to take the steps that you've already announced, the TLTROs, the ABS purchases, if you do those, before you consider anything else? Or would you be willing to step in with a QE program, for example, even before these other measures kick in? Thank you.

Draghi: Well, the answer to the second question is certainly if our medium to long-term assessment of inflation were to change, we certainly would use this broad asset purchase programme. So we don't have a schedule, but certainly, we first want to see the impact of this programme. We are convinced that, as I said at the beginning, the impact is going to be substantial. So I think someone asked me a question last time, saying what do you do next? I think I responded, if I had announced that we were lowering interest rates, would you ask when you lower it again? We're not going to say -- you see, that's what I meant by continued self-fulfilling expectations before. Maybe we should move to a six-month schedule rather than six-week schedule.

But no, the sequencing of the use of instruments is entirely dictated by the medium-term assessment of -- the assessment of medium-term outlook for inflation and price stability. There's no other consideration.

Question: My first one is also on the new schedule of the meetings. Does that have any implications for the rotation, as well, which will start at the beginning of next year? So is there a need to adapt the rules?

And the second one is also on the BIS report. The BIS also said that monetary policy is less effective in a balance sheet recession, and that it could do more harm than good if central banks try to do only more of the same. Could you follow this argument, or do you see a risk that you do too much, for example, to support credit?

Draghi: The answer to the first question is yes. That's partly why we are coordinating this exactly with the beginning of the rotation period, and the choice of the dates and everything has been also made with an eye to the rotation period.

On the second point, I think to some extent I've answered it before, but first of all, we completely agree that monetary policy is less effective when you are at a lower bound. We don't agree when it says that monetary policy would do more harm than good, because, as I said before, we think the monetary policy that's geared toward maintaining price stability has to have the stance that the Governing Council has decided with the present monetary policy. And the same thing is happening and has been said in all other monetary policy jurisdictions.

Are we ignoring the financial risk that could be produced because of the abundant liquidity, the very low risk spreads, risk premiums, the very low spreads, the very narrow spreads? No, we are not, and I've listed a series of measures that we've already taken. And with the entering into force of the Financial Stability Committee, there will be an explicit institutional attention to macro-prudential tools in the ESCB, so by the ECB and also by the national central banks and by the supervisors.

So the ECB and the ESCB and the supervisors in the SSM have been actively working -- and the ESRB, by the way -- have all been actively working to address this issue of financial stability risk within a monetary policy stance that remains firmly geared to restore price stability.

Question: To what extent is the Governing Council concerned by the scenario that the euro might become a so-called funding currency in so-called carry trades which may lead to its long-term depreciation, regardless of what actions the central bank takes?

And my second question, how can you be sure that the measures adopted recently will help credit flow to certain countries that need it most in light of the on-going fragmentation? Some hold the opinion that generating loans by lenders actually hinges more on demand than supply.

Draghi: On the second question, certainly, we asked this question. We ask this question all the time, just what are the main factors that would explain the weak credit growth that we've been seeing now for quite a long time? And we have basically a variety of instruments.

On top of having our internal analysis, we also have two surveys. One is the survey done with the Commission about the responses of the SMEs with respect to credit, and the second is the so-called bank lending survey, where it's banks that are being asked, what do you think are the main factors for the present credit trends?

Now, the two surveys, both of them basically say that it's both factors, both demand and supply. There has been some improvement on both accounts. However, the credit standards remain tighter on average than they used to be two years ago.

So we notice some improvement. In fact, you probably have noticed that also there is an improvement in the data showing a negative trend for growth but less negative than it was a month ago, two months ago, three months ago and so on. So you have a factor whereby the momentum of being negative is slowing down.

Also, looking at the disaggregated responses by the banks, you see that some factors have explained credit supply contraction in the past, like funding difficulties, for example, have seriously diminished or if not disappeared. The funding costs now are by and large the same across the euro area, so that is another interesting and positive phenomenon. There has been a narrowing of fragmentation on the funding side -- also on the lending side.

On the lending rates, there has been a narrowing of lending rates, but still, the differences remain still sizable. Within this picture, one has also to look at another type of fragmentation, which is in a sense horizontal -- namely, large corporates pay much lower rates to borrow money from the banks or from the capital markets than SMEs. And this is true everywhere, but of course it's truer for stressed countries.

So there are -- I would say, to summarise this -- certain very timid signs of improvement, but we are still witnessing low, low credit flows. I may also add another thing, however, that when you add to bank credit flows, other sources of external financing by the companies -- namely, debt issuance on capital markets and equity issuance -- you see that the decline in bank lending has been compensated by equity and bond issuance. And this has been true now for several months.

Again, on one hand, this is positive. On the other, we know that SMEs aren't doing any of these two things. In other words, usually, an SME is not able to issue bonds on the capital market, and you don't see much of equity issuance by SMEs in general. So that's what I can say about the credit markets.

On the first question, I'm not sure I got your question, I have to confess. Can you repeat it, please?

Question: My first question was some analysts pointed that the euro may become the funding currency in so-called carry trades, and it would basically lead to its depreciation in the long-term horizon. So to what extent was the Governing Council concerned by the scenario in the discussion?

Draghi: I have to say, we haven't actually considered this as an explicit policy issue so far.

Question: If you have every six weeks a meeting on monetary policy, does it mean you still have other internal meetings on non monetary affairs?

Second question, the ESRB has recently published a report called "Is Europe Overbanked," and basically, they said the European banking system is too fat and kind of dangerous. Do you agree?

Draghi: On the first point, the answer is yes. We will continue having exactly the number of internal meetings as adapted to the new schedule. And also, let me add that we have a new schedule for monetary policy meetings, but as it has always been the case in the past, we can always meet when and if needed on top of the foreseen schedule.

I have seen that paper, and certainly it's a very, very well written, designed and conceived paper. It's certainly worthwhile considering it seriously, and we are all looking at that. It's something, it's very hard to say do I agree or not, but certainly banks have especially -- well, all banks, really, are the product of history, of institutions, of a series of phenomena that have been stratifying one on top of the other.

So would a significant restructuring effort, going through mergers, acquisitions, resolutions -- would this be inappropriate? One can't really rule this out. The need for this, one can certainly not rule it out. So it's something. The paper definitely poses an interesting question that will require an appropriate analysis.

Whether the ECB or the supervisors or the ESRB are the right authorities to produce such a change, this is a different issue, and I don't think they would be the immediate actors in this process.

Comentarii

http://gyerekulesshop.hu/uzletek/statistics/AId1MA.php

It is learned that the defendant has now appealed.Tang Dynasty woman wearing flat shoes Ma, Po, leather and other textures. Prepared with twine called hemp shoes shoes, also known as line shoes, Astana Tombs, such as a pair of hemp shoes, thick crust with a thick hemp rope woven from fine linen and woven upper. [url=http://gyerekulesshop.hu/uzletek/statistics/AId1MA.php][/url]

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

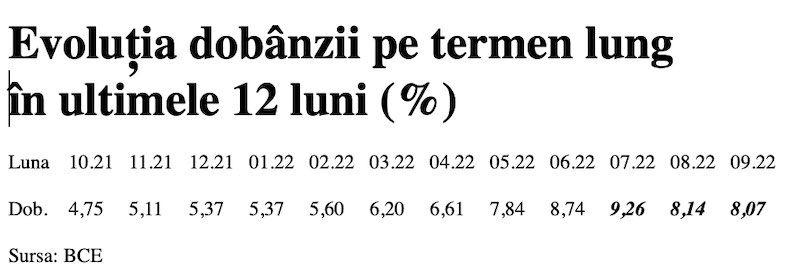

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

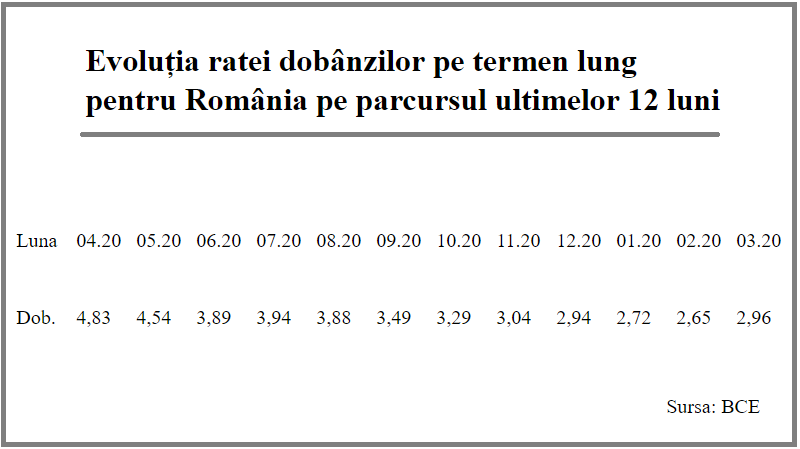

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent după primele două luni, mai mare cu 25%

- Deficitul contului curent, -0,39% din PIB după prima lună a anului

- Deficitul contului curent, redus cu 17%

- Inflatia a încheiat anul 2023 la 6,61%, semnificativ sub prognoza oficială

- Deficitul contului curent, redus cu o cincime după primele zece luni ale anului

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

- CEC Bank a preluat Fondul de Garantare a Creditului Rural

- BCR aproba credite online prin aplicatia George, dar contractele se semneaza la banca

- Aplicatia Eximbank, indisponibila temporar

Analize economice

- Rezultatul economic pe 2023, tot +2,1% dar cu 7 miliarde lei mai mare

- România - prima în UE la inflație, prin efect de bază

- Deficitul comercial lunar a revenit peste cota de 2 miliarde euro

- România, 78% din media UE la PIB/locuitor în 2023

- România - prima în UE la inflație, prin efect de bază

Ministerul Finantelor

- Datoria publică, imediat sub pragul de 50% din PIB la începutul anului 2024

- Deficitul bugetar, deja -1,67% din PIB după primele două luni

- Datoria publică, sub pragul de 50% din PIB la finele anului 2023

- Deficitul bugetar, din ce în ce mai mare la început de an

- Deficitul bugetar după 8 luni, încă mai mare față de rezultatul din anul trecut

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

- Taxa de reziliere a abonamentului Vodafone inainte de termen este ilegala (decizia definitiva a judecatorilor)

Stiri economice

- România, total în afara țărilor similare cu deficitul de cont curent

- Producția industrială pe februarie, cu aproape 7% sub cea din urmă cu cinci ani

- Inflația anuală a revenit la nivelul de la finele anului anterior

- Pensia reală de asigurări sociale de stat a crescut anul trecut cu 2,9%

- Producția de cereale boabe pe 2023, cu o zecime mai mare față de anul precedent

Statistici

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

- România, pe ultimul loc în UE la evoluția productivității muncii în agricultură

- INS: Veniturile romanilor au crescut anul trecut cu 10%. Banii de mancare, redistribuiti cu precadere spre locuinta, transport si haine

- Inflatia anuala - 13,76% in aprilie 2022 si va ramane cu doua cifre pana la mijlocul anului viitor

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

- O firma care a facut un schimb valutar gresit s-a inteles cu banca, prin intermediul CSALB

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Comerțul cu amănuntul, în expansiune la început de an

- România, pe locul 2 în UE la creșterea comerțului cu amănuntul în ianuarie 2024

- Comerțul cu amănuntul, în creștere cu 1,9% pe anul 2023

- Comerțul cu amănuntul, în creștere pe final de an

- Comerțul cu amănuntul, stabilizat la +2% față de anul anterior

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

Refuz de plată la o benzinărie suma de 103 euro

Mi s-au retras de două ori suma de 48 euro și suma de 103 euro suma corectă este de 48 de euro ... detalii

-

nevoia de banci

De ce credeti ca acum nu mai avem nevoie de banci si firme de asigurari? Pentru ca acum avem ... detalii

-

Mda

ACUM nu e nevoie de asa ceva .. acum vreo 20 de ani era nevoie ... ACUM de fapt nu mai e asa multa ... detalii

-

oprire pe salariu garanti bank

mi sa virat 2500de lei din care a fost oprit 850 de lei urmand sa mi se deblocheze restul sumei ... detalii

-

Amânare rate

Buna ziua, Am rămas în urma cu ratele , va rog frumos sa ma ajutați cumva , soțul a pierdut ... detalii