Mario Draghi: The state and prospects of the euro area recovery

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2016-11-20 10:25

Speech by Mario Draghi, President of the ECB, at the European Banking Congress, Frankfurt, 18 November 2016

Since the onset of the global financial crisis, 2016 has been the first full year where GDP in the euro area has been above its pre-crisis level. It has taken around 7.5 years to get there.

The economy is now recovering at a moderate, but steady, pace. Employment has grown by more than four million since its trough in 2013. And the recovery has become more broad-based, with less difference in economic performance across countries.

What we have now to ask is what are the factors that have allowed the recovery to gather steam, and whether we have reason to believe that they are sufficient to deliver a sustained adjustment in the path of inflation.

We have witnessed many encouraging developments, not least the healing of the euro area banking sector, which has allowed credit growth to turn positive again and monetary policy transmission to strengthen. This is a necessary condition for a full return to macro-economic and price stability.

But despite the uplift to prices provided by the gradual closing of the output gap, a sustained adjustment in the path of inflation still relies on the continuation of the current, unprecedented financing conditions. It is for this reason that we remain committed to preserving the very substantial degree of monetary accommodation, which is necessary to secure a sustained convergence of inflation towards level below, but close to, 2% over the medium-term.

What I would like to do in my remarks today is explain these perspectives – the factors that have put the euro area economy on a stronger footing, but also the reasons why we cannot yet drop our guard.

New factors making the euro area economy more robust

The first development that gives us comfort is the improving solvency of the banking sector.

We need a strong banking sector to support the economy through the recovery. But if there is one lesson we can draw from the past decade, it is that to be genuinely robust, the banking sector must be well-regulated. Indeed, there is a widespread agreement that one of the main causes of the global financial crisis was the excessive deregulation of the financial sector in the previous two decades.

The financial origins of the crisis explain in turn the slowness of the economic recovery. Banks that overextended credit in the upswing had to clean up their balance sheets and strengthen their capital. Firms and households that took on excessive debt had to deleverage. And that combination depressed both credit supply and demand.

So the re-regulation of the financial sector is in fact a part of the growth agenda. And major progress has now been made in redressing the mistakes of the pre-crisis era.

The global regulatory agenda, steered by the G-20, has made the sector considerably more robust in terms of capital, leverage, funding and risk-taking. Common Equity Tier 1 ratios in the euro area have improved substantially, rising from less than 7% for significant banking groups in 2008 to more than 14% today. Leverage ratios are now close to 4% for large banks. The Liquidity Coverage Ratio was implemented last year, and most euro area banks are already complying with the Net Stable Funding Ratio ahead of its implementation in 2018.

It is true that this regulatory agenda, which has evolved profoundly in its design over the past eight years, may also have created some uncertainties, for instance over steady state capital levels, which are reflected in bank share prices. Indeed, uncertainty over future capital requirements can give rise to a risk premium, which weighs on banks’ cost of finance and acts as a deterrent to expanding activities or supplying credit to the economy.

So now is the time to finalise the regulatory agenda and enter a period of stability. The focus should be on implementation, not on new design. Regulatory measures should be implemented in a balanced way that ensures a level playing-field globally. And while marginal adjustments are possible, there should be no rolling back on what has been decided.

Re-regulation has led to welcome improvements in bank solvency. Meanwhile, asset quality has also improved. The non-performing loan (NPL) ratio has been decreasing in the euro area, even if modestly. Critical in this context was the Comprehensive Assessment of bank balance sheets – including an asset quality review of great depth – which encouraged banks to frontload the strengthening of their balance sheet. While NPLs remain high in some countries, the problem today is more related to profitability than to the robustness of balance sheets, since coverage ratios are close to 50% and much of the remainder is collateralised.

All this progress has gone hand-in-hand with a steadying economic recovery. Increased banking sector resilience has helped shield the recovery from external shocks and sustain its internal momentum. The banking system has been able to weather, among other things, the crisis in emerging market economies, the collapse in oil and commodity prices, and the consequences of the UK referendum. And healthier banks have provided the necessary supply of credit to maintain the pace of the recovery.

The easing in credit supply conditions has been visible in both lending rates and lending volumes. Since mid-2014, bank lending rates have fallen by almost 100 basis points for both euro area households and corporates. Small and medium-sized enterprises have benefitted from even larger declines. Lending volumes, in turn, have posted positive growth rates for households since end-2014, and for non-financial corporations since the last quarter of 2015, following multi-year declines.

And financing conditions have improved in capital markets too, which has been followed by a pick-up in corporate bond issuance.

This credit reversal has in turn supported a second benign characteristic of the recovery: the fact that it has become increasingly driven by domestic sources of growth.

Domestic demand has now replaced foreign demand as the main driver of growth. Over the past two years, domestic demand has on average added more than a percentage point to GDP growth, supported by very accommodative financing conditions. By contrast, net exports, which were a key growth engine for most of the crisis period, have barely contributed to GDP growth since end-2013 as the global environment has deteriorated.

This shift in the composition of growth is important, from an inflation perspective, since it makes the recovery in the euro area less vulnerable to external shocks. Indeed, domestic strength has helped insulate the euro area against recent global weakness, which otherwise would have dragged the recovery off track – and with it, the expected pick-up in the path of inflation.

The domestic picture is also contributing to a third encouraging development: the strong rebound in employment. This has been driven by a striking reconnection between GDP and employment growth in recent years.[1] The temporary post-Lehman rebound in 2010-11 was essentially a jobless recovery. The current recovery, however, has reduced the unemployment rate from more than 12% in 2013 to 10% today. And, besides lower unemployment, the overall labour force has expanded as well in recent years, reflecting increasing labour participation rates.[2]

A faster return to full employment – or what economists call the “non-accelerating inflation rate of unemployment” – is clearly supportive of price stability, since it heralds a tighter labour market and stronger wage pressures. And while those pressures might be somewhat offset by the increasing number of people entering the labour force as the recovery strengthens, a larger workforce will ultimately support both supply – by raising potential growth – and demand.

With strengthening labour market prospects, existing employees can be reassured of their earnings prospects and revive their spending plans with greater confidence; and new recruits can satisfy some of the pent-up demand they accumulated while unemployed. The elasticity of aggregate consumption to new hires is particularly large.

As such, these labour market trends represent a key factor in preserving growth and inflation momentum in conditions where global demand may become a less dependable engine of growth.

Factors warranting prudence

We have therefore every reason to be more confident in the strength of the recovery than we were one year ago. But we cannot be sanguine over the economic outlook.

Besides the geopolitical risks that remain prevalent, there are indeed three factors that warrant caution: the profitability of euro area banks, the relative weakness of inflation dynamics, and the dependence of the recovery on accommodative monetary policy.

Even though the euro area banking system is today more resilient, its profitability remains a challenge – one that is weighing on bank share prices and raising the cost banks face when raising equity. There has in fact been a negative gap between euro area banks’ return on equity and their cost of equity since the 2008 financial crisis.

While the level of bank equity prices is not per se a matter for policymakers, insofar as it raises financing costs for banks, it could ultimately curtail lending to the real economy and hold back the recovery.

One of the factors weighing on profitability is the low growth and low inflation environment, which translates into lower levels of policy interest rates. But legacy and structural challenges are also at play, which banks and policymakers can and should address.

Where the legacy stock of NPLs is depressing profitability, key is to create an environment where the resolution of bad loans can be accelerated. And where profitability is being affected by structural issues, such as overcapacity and inefficient cost structures, rationalisation and consolidation must form part of the answer. Indeed, such inefficiencies may have been exposed by the low interest rate environment, but they have certainly not been created by it.

A second reason to remain alert is that despite the recovery in growth and employment, the persisting output gap is still keeping inflation dynamics weak. The October inflation rate stood at 0.5%. While this marks the highest level recorded in almost two years, it remains far below the ECB’s objective. And while we expect headline inflation to continue rising over the coming months, much of this increase will be driven by statistical factors related to the mechanical unwinding of the extreme oil price declines a year ago. We do not yet see a consistent strengthening of underlying price dynamics.

Our objective is – and will remain – a rate of inflation below, but close to, 2% over the medium term. Going forward, our assessment will depend on whether we see a sustained adjustment in the path of inflation towards that objective. And that means that inflation convergence towards 2% is durable, even with a reduction in monetary accommodation. Inflation dynamics, in other words, need to be self-sustained.

And this brings me to the third factor which calls for prudence over the outlook: the fact that the euro area recovery still relies to a considerable degree on accommodative monetary policy. The recovery in credit is being facilitated by a more resilient banking sector, but the impetus comes from our monetary policy.

Our measures and their effective transmission underpin our outlook for growth and inflation. According to staff estimates, our measures will raise the inflation rate by more than half a percentage point, on average, over 2016 and 2017. And they will contribute to increasing real euro area GDP growth by more than one and a half percentage points cumulatively between 2015 and 2018. In other words, monetary policy remains a key ingredient in the reflation scenario we foresee for the euro area in the coming years.

Conclusion

So even if there are many encouraging trends in the euro area economy, the recovery remains highly reliant on a constellation of financing conditions that, in turn, depend on continued monetary support. The ECB will continue to act, as warranted, by using all the instruments available within our mandate to secure a sustained convergence of inflation towards a level below, but close to 2%.

We also have to recognise that we operate under a still significant degree of uncertainty. Whether the economic recovery becomes more solid, and how quickly inflation dynamics become more self-sustained, depends not just on the current monetary policy stance, but also on other policies, as I have discussed on several other occasions. Restoring a sense of direction – and therefore confidence – would be the simplest and yet most powerful way to deliver economic stimulus.

Source: ECB statement

Taguri: online banking BT Direct European Central Bank (ECB) comisioane card reclamatie Vodafone EURIBOR

Comentarii

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

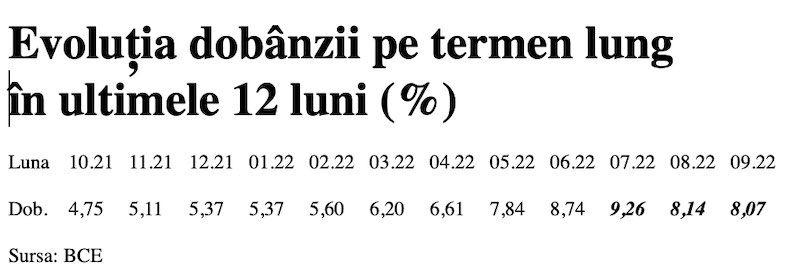

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

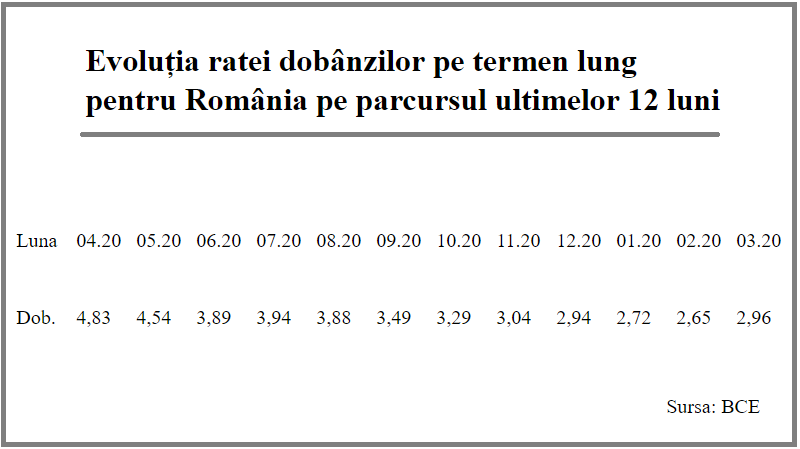

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent, aproape 20 miliarde euro după primele nouă luni

- Deficitul contului curent, aproape 18 miliarde euro după primele opt luni

- Deficitul contului curent, peste 9 miliarde euro pe primele cinci luni

- Deficitul contului curent, 6,6 miliarde euro după prima treime a anului

- Deficitul contului curent pe T1, aproape 4 miliarde euro

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Cate reclamatii primeste Intesa Sanpaolo Bank si cum le gestioneaza

- Platile instant, posibile la 13 banci

- Aplicatia CEC app va functiona doar pe telefoane cu Android minim 8 sau iOS minim 12

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

Analize economice

- România, „lanterna roșie” a cheltuielilor pentru cercetare-dezvoltare în UE

- Deficitul contului curent, peste 24 miliarde euro după primele zece luni

- Deficit comercial record în octombrie 2024

- Productivitatea în comerț, peste cea din industrie

- -6,2% din PIB, deficit bugetar după zece luni

Ministerul Finantelor

- Datoria publică, 51,4% din PIB la mijlocul anului

- Deficit bugetar de 3,6% din PIB după prima jumătate a anului

- Deficit bugetar de 3,4% din PIB după primele cinci luni ale anului

- Deficit bugetar îngrijorător după prima treime a anului

- Deficitul bugetar, -2,06% din PIB pe primul trimestru al anului

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- ANPC pierde un proces cu Intesa si ARB privind modul de calcul al ratelor la credite

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

Stiri economice

- Inflația anuală a crescut la 5,11%, prin efect de bază

- Datoria publică, 54,4% din PIB la finele lunii septembrie 2024

- România, tot prima dar în trendul UE la inflația anuală

- Datoria publică, 52,7% din PIB la finele lunii august 2024

- -5,44% din PIB, deficit bugetar înaintea ultimului trimestru din 2024

Statistici

- România, pe locul trei în UE la creșterea costului muncii în T2 2024

- Cheltuielile cu pensiile - România, pe locul 19 în UE ca pondere în PIB

- Dobanda din Cehia a crescut cu 7 puncte intr-un singur an

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- Sistemul bancar romanesc este deosebit de bine pregatit pentru orice fel de socuri

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Comerțul cu amănuntul - în creștere cu 8% pe primele 10 luni

- Deficitul balanței comerciale la 9 luni, cu 15% mai mare față de aceeași perioadă a anului trecut

- Producția industrială, în scădere semnificativă

- Pensia reală, în creștere cu 8,7% pe luna august 2024

- Avansul PIB pe T1 2024, majorat la +0,5%

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

împrumut

Vreau să apreciez pe Karin Sabine un împrumut de 9000€ pentru mine. Dacă aveți nevoie de un ... detalii

-

împrumut

Vreau să apreciez pe Karin Sabine un împrumut de 9000€ pentru mine. Dacă aveți nevoie de un ... detalii

-

Buna ziua! Am nevoie de ajutor!

Buna ziua! Am trimis activare cont si imi scrie ca au expediat QR Cod pe posta dar nu mia venit ... detalii

-

Înșelătorie

Mare atenție la firma vex group, te pune să investești 250 € în Forex, câștigi ceva și ... detalii

-

interdictie conturi ING

Buna ziua, o situatie ca cele de mai sus am patit si eu, cu diferenta ca Revolut a deblocat contul ... detalii