Mario Draghi: Introductory statement to the press conference

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2016-09-08 17:38

Mario Draghi: Introductory statement to the press conference:

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB

Frankfurt am Main, 8 September 2016

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the Commission Vice-President, Mr Dombrovskis.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at present or lower levels for an extended period of time, and well past the horizon of our net asset purchases.

Regarding non-standard monetary policy measures, we confirm that the monthly asset purchases of €80 billion are intended to run until the end of March 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim.

Today, we assessed the economic and monetary data which had become available since our last meeting and discussed the new ECB staff macroeconomic projections.

Overall, while the available evidence so far suggests resilience of the euro area economy to the continuing global economic and political uncertainty, our baseline scenario remains subject to downside risks.

Our comprehensive policy measures continue to ensure supportive financing conditions and underpin the momentum of the euro area economic recovery. As a result, we continue to expect real GDP to grow at a moderate but steady pace and euro area inflation to rise gradually over the coming months, in line with the path already implied in our June 2016 staff projections.

The Governing Council will continue to monitor economic and financial market developments very closely. We will preserve the very substantial amount of monetary support that is embedded in our staff projections and that is necessary to secure a return of inflation to levels below, but close to, 2% over the medium term. If warranted, we will act by using all the instruments available within our mandate. Meanwhile, the Governing Council tasked the relevant committees to evaluate the options that ensure a smooth implementation of our purchase programme.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.3%, quarter on quarter, in the second quarter of 2016, after 0.5% in the first quarter. Incoming data point to ongoing growth in the third quarter of 2016, at around the same rate as in the second quarter.

Looking ahead, we continue to expect the economic recovery to proceed at a moderate but steady pace.

Domestic demand remains supported by the pass-through of our monetary policy measures to the real economy. Favourable financing conditions and improvements in the demand outlook and in corporate profitability continue to promote a recovery in investment. Sustained employment gains, which are also benefiting from past structural reforms, and still relatively low oil prices provide additional support for households’ real disposable income and thus for private consumption.

In addition, the fiscal stance in the euro area is expected to be mildly expansionary in 2016 and to turn broadly neutral in 2017 and 2018. However, the economic recovery in the euro area is expected to be dampened by still subdued foreign demand, partly related to the uncertainties following the UK referendum outcome, the necessary balance sheet adjustments in a number of sectors and a sluggish pace of implementation of structural reforms.

The risks to the euro area growth outlook remain tilted to the downside and relate mainly to the external environment.

This assessment is broadly reflected in the September 2016 ECB staff macroeconomic projections for the euro area, which foresee annual real GDP increasing by 1.7% in 2016, by 1.6% in 2017 and by 1.6% in 2018. Compared with the June 2016 Eurosystem staff macroeconomic projections, the outlook for real GDP growth has been revised downwards slightly.

According to Eurostat’s flash estimate, euro area annual HICP inflation in August 2016 was 0.2%, unchanged from July. While annual energy inflation continued to rise, services and non-energy industrial goods inflation turned out to be slightly lower than in July.

Looking ahead, on the basis of current oil futures prices, inflation rates are likely to remain low over the next few months before starting to pick up towards the end of 2016, in large part owing to base effects in the annual rate of change of energy prices.

Supported by our monetary policy measures and the expected economic recovery, inflation rates should increase further in 2017 and 2018.

This pattern is also reflected in the September 2016 ECB staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 0.2% in 2016, 1.2% in 2017 and 1.6% in 2018. In comparison with the June 2016 Eurosystem staff macroeconomic projections, the outlook for HICP inflation is broadly unchanged.

Turning to the monetary analysis, broad money (M3) continued to increase at a robust pace in July 2016, with its annual rate of growth standing at 4.8%, after 5.0% in June. As in previous months, annual growth in M3 was mainly supported by its most liquid components, with the narrow monetary aggregate M1 expanding at an annual rate of 8.4% in July, after 8.7% in June.

Loan dynamics followed the path of gradual recovery observed since the beginning of 2014. The annual rate of change of loans to non-financial corporations increased to 1.9% in July 2016, compared with 1.7% in June. The annual growth rate of loans to households remained stable at 1.8% in July. Although developments in bank credit continue to reflect the lagged relationship with the business cycle, credit risk and the ongoing adjustment of financial and non-financial sector balance sheets, the monetary policy measures in place since June 2014 are increasingly filtering through to support borrowing conditions for firms and households and thereby credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need to preserve the very substantial amount of monetary support that is necessary in order to secure a return of inflation rates towards levels that are below, but close to, 2% without undue delay.

Monetary policy is focused on maintaining price stability over the medium term and its accommodative stance supports economic activity. As emphasised repeatedly by the Governing Council, and as strongly echoed in both European and international policy discussions, in order to reap the full benefits from our monetary policy measures, other policy areas must contribute much more decisively, both at the national and at the European level.

The implementation of structural reforms needs to be substantially stepped up to reduce structural unemployment and boost potential output growth in the euro area. Structural reforms are necessary in all euro area countries. The focus should be on actions to raise productivity and improve the business environment, including the provision of an adequate public infrastructure, which are vital to increase investment and boost job creation.

The enhancement of current investment initiatives, including the extension of the Juncker plan, progress on the capital markets union and reforms that will improve the resolution of non-performing loans will also contribute positively to this objective.

In an environment of accommodative monetary policy, the swift and effective implementation of structural reforms will not only lead to higher sustainable economic growth in the euro area but will also make the euro area more resilient to global shocks.

Fiscal policies should also support the economic recovery, while remaining in compliance with the fiscal rules of the European Union. Full and consistent implementation of the Stability and Growth Pact over time and across countries remains crucial to ensure confidence in the fiscal framework. At the same time, all countries should strive for a more growth-friendly composition of fiscal policies.

We are now at your disposal for questions.

Source: ECB statement

Taguri: online banking BT Direct European Central Bank (ECB) Banca Centrala Europeana (BCE) amanare rate credite reclamatie Vodafone

Comentarii

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

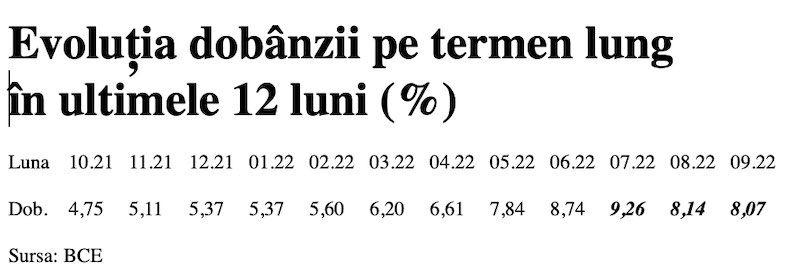

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

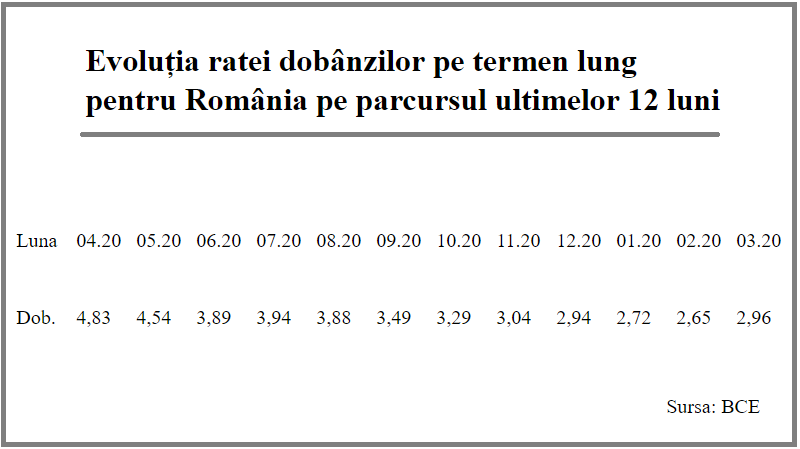

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Profil de Bancher

-

Catalina Molnar, economist-sef

UniCredit Bank

Catalina Molnar, noul economist-sef al UniCredit ... vezi profil

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent, aproape 20 miliarde euro după primele nouă luni

- Deficitul contului curent, aproape 18 miliarde euro după primele opt luni

- Deficitul contului curent, peste 9 miliarde euro pe primele cinci luni

- Deficitul contului curent, 6,6 miliarde euro după prima treime a anului

- Deficitul contului curent pe T1, aproape 4 miliarde euro

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Cate reclamatii primeste Intesa Sanpaolo Bank si cum le gestioneaza

- Platile instant, posibile la 13 banci

- Aplicatia CEC app va functiona doar pe telefoane cu Android minim 8 sau iOS minim 12

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

Analize economice

- România, „lanterna roșie” a cheltuielilor pentru cercetare-dezvoltare în UE

- Deficitul contului curent, peste 24 miliarde euro după primele zece luni

- Deficit comercial record în octombrie 2024

- Productivitatea în comerț, peste cea din industrie

- -6,2% din PIB, deficit bugetar după zece luni

Ministerul Finantelor

- Datoria publică, 51,4% din PIB la mijlocul anului

- Deficit bugetar de 3,6% din PIB după prima jumătate a anului

- Deficit bugetar de 3,4% din PIB după primele cinci luni ale anului

- Deficit bugetar îngrijorător după prima treime a anului

- Deficitul bugetar, -2,06% din PIB pe primul trimestru al anului

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- ANPC pierde un proces cu Intesa si ARB privind modul de calcul al ratelor la credite

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

Stiri economice

- Inflația anuală a crescut la 5,11%, prin efect de bază

- Datoria publică, 54,4% din PIB la finele lunii septembrie 2024

- România, tot prima dar în trendul UE la inflația anuală

- Datoria publică, 52,7% din PIB la finele lunii august 2024

- -5,44% din PIB, deficit bugetar înaintea ultimului trimestru din 2024

Statistici

- România, pe locul trei în UE la creșterea costului muncii în T2 2024

- Cheltuielile cu pensiile - România, pe locul 19 în UE ca pondere în PIB

- Dobanda din Cehia a crescut cu 7 puncte intr-un singur an

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- Sistemul bancar romanesc este deosebit de bine pregatit pentru orice fel de socuri

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Comerțul cu amănuntul - în creștere cu 8% pe primele 10 luni

- Deficitul balanței comerciale la 9 luni, cu 15% mai mare față de aceeași perioadă a anului trecut

- Producția industrială, în scădere semnificativă

- Pensia reală, în creștere cu 8,7% pe luna august 2024

- Avansul PIB pe T1 2024, majorat la +0,5%

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

împrumut

Vreau să apreciez pe Karin Sabine un împrumut de 9000€ pentru mine. Dacă aveți nevoie de un ... detalii

-

împrumut

Vreau să apreciez pe Karin Sabine un împrumut de 9000€ pentru mine. Dacă aveți nevoie de un ... detalii

-

Buna ziua! Am nevoie de ajutor!

Buna ziua! Am trimis activare cont si imi scrie ca au expediat QR Cod pe posta dar nu mia venit ... detalii

-

Înșelătorie

Mare atenție la firma vex group, te pune să investești 250 € în Forex, câștigi ceva și ... detalii

-

interdictie conturi ING

Buna ziua, o situatie ca cele de mai sus am patit si eu, cu diferenta ca Revolut a deblocat contul ... detalii