Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2017-08-27 11:18

Sustaining openness in a dynamic global economy

Speech by Mario Draghi, President of the ECB, at the Economic Policy Symposium of the Federal Reserve Bank of Kansas City, Jackson Hole, 25 August 2017

The global recovery is firming up. In some countries like the United States, this process has been visible for some years, in others like Europe and Japan, the consolidation of the recovery is at an earlier stage. So it is fitting that our discussions are now focusing not only on how to stabilise the economy, but also on how to make it more dynamic – while at the same time improving people welfare. At the centre of this debate is the question of how to raise potential output growth, which has slowed from around 2% in OECD countries in 2000 to around 1% today.[1]

Without stronger potential growth, the cyclical recovery we are now seeing globally will ultimately converge downwards to those slower growth rates. Slower growth will in turn make it harder to work through the debt and demographic challenges facing many advanced economies.

With the population growth rate in those economies projected to slow, the burden of raising potential growth must fall on productivity. There are a number of areas in which domestic policies can encourage an upward shift in productivity growth, such as competition, research and development, and insolvency regimes.

But when thinking about the global economy, one of the key ingredients for raising productivity is openness. Open trade, investment and financial flows play a key role in the diffusion of new technologies across borders that drive forward efficiency improvements.

The social consensus on open markets has, however, been weakening in recent years. This is driven not so much by a belief that open markets no longer create wealth, but by the perception that the collateral effects of openness outweigh its benefits. People are concerned about whether openness is fair, whether it is safe and whether it is equitable.

As Karl Polanyi observed many years ago, if the dislocation created by an open market goes beyond a certain point, protectionism is society natural response.[2]

So a central element of efforts to raise productivity growth – and build a dynamic global economy – must involve responding to these concerns about openness. And this is a feat countries cannot accomplish by themselves.

Although domestic welfare policies are, of course, essential to the task, a commitment to working together through multilateral institutions is just as important.

This is because fears about fairness, safety and equity ultimately reflect a lack of trust in other countries regulation and enforcement. One of the main reasons why multilateral institutions exist is to create regulatory convergence, and therefore to increase trust between countries.[3] And perhaps the most important area where this applies today is global financial sector regulation.

Openness as the key to a dynamic global economy

One of the key questions facing the global economy is whether the trend towards ever greater economic openness, which has defined the last three decades, is coming to an end. Temporary trade barriers have indeed risen from covering around 1% of products in 2000 to more than 2.5% today, with the crisis accelerating this pattern. The same is true of anti-dumping actions.[4]

That said, at the global level openness is still viewed favourably; three-quarters of people consider growing trade and business ties with other countries to be a positive trend. But those polled in rich countries are more negative than in the pre-crisis period.[5]

Given the established gains of trade, this is plainly a concerning trend for the global economy. International trade results in a more efficient use of production factors and in specialisation where comparative advantage exists, thereby raising productivity growth.[6] And welfare gains from trade for firms and consumers follow from the wider availability of cheaper and better quality products.[7]

Moreover, for advanced economies the importance of trade may actually be growing. As economies converge towards the global technological frontier, innovation becomes more important for sustained productivity growth. And as OECD research has shown, openness to trade is a crucial factor in enabling an economy to benefit from frontier innovation. [8]

According to OECD estimates, in the case of a 2% acceleration in multi-factor productivity (MFP) growth in a frontier economy, the productivity spillover will be 0.3 percentage points higher for a country that trades intensively with the frontier economy than for one which trades less intensively. To put this in context, MFP growth has averaged only around 0.5% in OECD countries since 2000.[9]

Thus a turn towards protectionism would pose a serious risk for continued productivity growth and potential growth in the global economy. And this risk is particularly acute in the light of the structural challenges facing advanced economies.

Old-age dependency ratios are rising, putting more pressure on public finances. By 2025 there will be 35 people aged 65 and over for every 100 persons of working age in OECD countries, compared with 14 in 1950.[10] At the same time, public debt levels have surged in those countries from 56% of GDP in 2007 to around 87% today.[11] Only higher potential growth can provide a lasting solution.

So, clearly, to foster a dynamic global economy we need to resist protectionist urges. But to do so, we also need to identify how best to respond to protectionism.

The role of multilateral cooperation in making openness sustainable

Much has been written over the past few years about the negative effects of free trade and the need to pay more attention to those who benefit less from it. The debate has typically focused on the extent to which welfare policies can be used to share the gains of trade more evenly.

Though this is a complex issue,[12] I have no doubt that making better use of public policies to support the more vulnerable members of society, not just financially but also through education and retraining, is a vital part of the equation. More work needs to be done in this area and it is important to learn from best policy practices.

But the other key question is: how can we work together to make openness sustainable? What role can multilateral cooperation play towards this goal? This is the angle I would like to address today. Its importance becomes clear when one thinks about the three main areas of concern that people have about open markets that I mentioned earlier.

First, there is the concern about whether openness is fair – i.e. whether all are playing by the same rules and applying the same standards. This manifests itself in fears about currency manipulation by trading partners, dumping practices and lack of reciprocal market access.

Second, there is the concern about whether openness is safe – i.e. whether it exposes people to harmful spillovers from abroad. This is perhaps most visible, at least for economists, in the case of cross-border capital flows[13], but it also applies in areas such as agriculture and biotechnology.

Third, there is the concern about whether openness is equitable – that is, whether it disproportionately benefits some groups in society over others. Though it is not straightforward to disentangle the effects of trade and technology on inequality – and they may in fact be linked[14]– the perception that openness contributes to inequality has become more widespread.

In each case, multilateral cooperation, leading to regulatory convergence, is a precondition for addressing the underlying causes of these concerns. To demonstrate this, let me draw on our experience of managing openness within the European Union.[15]

As regards fairness, the point is obvious: regulatory convergence provides the strongest assurance that the playing field is level right across the European market. This is why, as borders have opened within Europe, common supranational powers of legislation and enforcement have strengthened in parallel.

For example, the Single European Act in 1986 not only launched the single market, it also substantially extended the powers of the EU to make laws, the role of the European courts to rule on them, and the powers of the Commission to execute them. The logic was that a single market could only be sustainable over time if all participants could be certain that they faced the same rules, and had recourse to the same courts in the case of infractions.

Despite the political events of last year, this symmetry between regulatory convergence and market deepening has, by and large, been a success. In fact, the free movement of people, goods and services within Europe is regularly mentioned in polls as one of the two most positive aspects of the EU, the other being peace among its Member States.[16]

Similarly, what has permitted the Single Market to survive various financial and consumer protection crises is its ability to restore safety by adapting market-wide regulation and enforcement.

To give an illustration, the internal market for frozen foods overcame the mis-selling scandal of 2013, when horsemeat was sold as beef, in large part because it was met with an improved food labelling and EU-wide inspection regime that restored trust. By contrast, a perceived lack of regulatory convergence between the EU and other countries, especially regarding food safety, is one reason for opposition to preferential trade agreements, such as the TTIP.

More fundamentally, following the sovereign debt crisis, the euro area experienced first-hand the risks of a diverging supervisory and regulatory framework for cross-border finance – and faced a serious threat of financial market fragmentation when those flows reversed.

Safety was restored by elevating supervision and resolution to the European level with the banking union. This was key to re-establishing trust in the banking system and reviving cross-border capital flows within Europe. These are only the first steps, but the direction of travel has been drawn.

When it comes to the effects of openness on equity, it is admittedly less obvious how multilateral cooperation represents a solution to the fears being expressed. As I said, such fears typically have to be addressed by national distributional policies. But there is also an important international dimension, in particular related to tax avoidance.

Indeed, the problem many have with openness is not just that it redistributes income between different social groups. Almost everything that happens in a market economy – skill-biased innovation, churning of firms – redistributes income in some way, and we have in place mechanisms to deal with those outcomes, such as tax systems.

Where trade may differ from these other market forces, however, is in the perception that, in Dani Rodrik words, it “undercuts the social bargains struck within a nation and embedded in its laws and regulations”.[17] For example, increasing openness to trade and finance is perceived by some to shift the burden of taxation from footloose capital to labour, or to create pressures to reduce labour protections to boost the competitiveness of domestic producers – the “race to the bottom”.

Such perceptions, and the sense of injustice they fuel, are deeply damaging to public faith in open markets – and this is where multilateral solutions can play a role.

Addressing tax arbitrage between jurisdictions, for instance, can clearly best be achieved by countries cooperating via international institutions. Likewise, taking a stand against race-to-the-bottom dynamics that threaten labour protections, calls for a common regulatory approach. Again, our experience in Europe offers some insights into how this can work, as well as into some of the difficulties involved.

Thanks to its common legal framework, the EU has successfully upheld labour standards even as its market has expanded to lower-income countries. The Single Market has no doubt prompted some relocation of jobs across countries, and this has at times triggered fears of “social dumping”.[18] But in fact openness has not fundamentally challenged labour protections.

One main reason for this is that safeguards central to the European social model have been progressively embedded in European law, ensuring gradual convergence in labour standards among EU countries. Thus, while there is still heterogeneity, the gap between them is narrowing.

Preferences about the degree and type of social and labour protection differ across the world, and I am not claiming that those in the EU should be a model for everybody. The point here is that through multilateral decision-making, the EU has successfully built and defended the single market, addressing the perception that openness is always a source of inequality.

At the same time, in areas where unanimous decision-making is more prevalent, Europe has not always used the potential of its multilateral structure to the same extent. This is the case, for instance, in combatting profit-shifting and tax avoidance, although progress is now being made,[19] which clearly chimes with the mood of EU citizens.[20]

In short, there are certain concerns about equity that can most effectively – and perhaps only – be addressed through multilateral actions. As such, in tandem with well-targeted welfare policies, they are a key part of the policy toolbox for making openness sustainable.

Implications for the global economy

Clearly, the European model involves several unique features. In particular, it depends on a relatively advanced political structure that helps reconcile multilateral cooperation with democratic control, which is difficult to replicate elsewhere. Still, EU countries are generally more open than other advanced economies and perhaps have fewer problems of skewed income distribution.[21] So what lessons can we draw for the global economy from our experience?

The most salient is that, at a time when disaffection with openness is growing, multilateral institutions become more, not less important. They provide the best platform to address concerns about openness without sacrificing open markets.

So organisations like the WTO, which make sure that trade is governed by rules and is subject to fair arbitration, remain vital to ensuring that global trade is perceived as fair and safe – while at the same time avoiding protectionism in disguise. And bodies that foster global cooperation, such as the G20, remain just as necessary to reconcile openness with equity. The OECD/G20 initiative to combat tax base erosion and profit-shifting is just one example of such cooperation.

That said – and going by our experience in Europe – the area where we need a special focus today is cross-border finance. Organisations that facilitate convergence in financial regulation and supervision, such as the Financial Stability Board and the Basel committees, are key in this context.

Within these committees, a substantial amount of work has been done since the crisis to strengthen microprudential regulation, as well as to design and calibrate macroprudential tools. This work has been essential for at least three reasons.

The first reason is that finance is the most mobile production factor, and therefore the most likely to cause dangerous spillovers. This makes convergence in financial regulation one of the most important components of a sustainable open economy.

And we should remember that diverging financial regulation would endanger not only financial openness, but also global trade, since they are often two sides of the same coin: finance and trade are complementary in spreading knowledge and underpinning global value chains. A striking feature of the global financial crisis was indeed the collapse in world trade: between the third quarter of 2008 and the second quarter of 2009 global trade volumes declined by approximately 15%.

The second reason is that we have only recently witnessed the dangers of financial openness combined with insufficient regulation. International financial flows both contributed to and propagated the global financial crisis and the ensuing collapse of trade, output and employment.

Financial integration only survived relatively unscathed because the global regulatory response was swift and decisive, creating a financial system that posed fewer risks to the world economy. Any reversal would call into question whether the lessons of the crisis have indeed been learnt – and thus whether financial integration can still be considered safe.

Third, financial regulation interacts critically with monetary policy. Lax regulation implies an underestimation by regulators of incentives which lead to behaviour that is individually profitable, but socially costly. Given the large collective costs that we have observed, there is never a good time for lax regulation. But there are times when it is especially inopportune.

Specifically, when monetary policy is accommodative, lax regulation runs the risk of stoking financial imbalances. By contrast, the stronger regulatory regime that we have now has enabled economies to endure a long period of low interest rates without any significant side-effects on financial stability[22], which has been crucial for stabilising demand and inflation worldwide.

With monetary policy globally very expansionary, regulators should be wary of rekindling the incentives that led to the crisis.

To design and agree, in reciprocal trust, a regulation that preserves financial stability without unnecessarily restricting the flow of credit to the economy, while revisiting the post-crisis regulatory framework where necessary, the FSB and the Basel committees remain essential. This is also because, for large economies, changes in domestic regulation have international consequences. Global financial conditions account for 20-40% of the variation in countries domestic financial conditions, as shown by recent research from the IMF.[23]

Conclusion

Let me conclude.

To inject more dynamism into the global economy we need to raise potential output growth, and to do so with ageing societies we need to lift productivity growth. For advanced economies that are close to the technological frontier, this depends crucially on openness to trade.

Yet openness to trade is under threat, and this means that policies aimed at answering this backlash are a vital part of the policy mix for dynamic growth. Some of those policies can be implemented domestically, but some can only be effectively enacted through multilateral cooperation.

Multilateral cooperation is crucial in responding to concerns about fairness, safety and also equity. By encouraging regulatory convergence, it helps protect people from the unwelcome consequences of openness. And protection ensures that we do not lapse into protectionism over time.

The European experience provides some insights into the opportunities and challenges involved. It also shows the importance of ensuring that, at all times, openness remains under democratic control. Multilateral institutions are necessarily staffed by experts. But it is essential that they always remain accountable to elected representatives who set the parameters and have the final say.

[1] Per capita potential output growth, OECD data.

[2] Polanyi, K. (1944), The Great Transformation.

[3] See, for example, Williamson, O. (1996), The Mechanisms of Governance.

[4] Bown, C.P. (2016), Global Antidumping Database, The World Bank; World Bank Temporary Trade Barriers Database.

[5] Pew Research Center (2014), “Faith and Skepticism about Trade, Foreign Investment”, September. However, a Pew Research Center poll released in August 2017 found that, in the context of immigration, 68% of Americans believe that “America openness to people from all over the world is essential to who we are as a nation”.

[6] The most recent review in the literature has been published by the IMF and confirms that international trade improves welfare and strengthens economic growth. See IMF (2016), “Global Trade: What is behind the slowdown?”, World Economic Outlook, Chapter 2, October.

[7] For more information on this topic, see Helpman and Krugman (1985), Grossman and Helpman (1991), Melitz(2003), Broda and Weinstein (2006), Melitz and Ottaviano, (2007), Antoniades (2015).

[8] Saia, A., Andrews, D. and Albrizio, S. (2015), “Productivity Spillovers from the Global Frontier and Public Policy: Industry-Level Evidence”, OECD Economics Department Working Papers, No 128.

[9] OECD data, unweighted average.

[10] OECD (2015), Pensions at a Glance 2015: OECD and G20 indicators, OECD Publishing, Paris.

[11] OECD data, unweighted average.

[12] See, for example, Antràs, P., de Gortari, A. and Itskhoki, O. (forthcoming), “Globalization, Inequality and Welfare”, Journal of International Economics.

[13] Broner, F. and Ventura, J. (2016), “Rethinking the Effects of Financial Globalisation”, Quarterly Journal of Economics, Vol. 131, Issue 3.

[14] For a review see Pavcnik, N. (2011), “Globalization and within-country income inequality”, in Bacchetta, M. and M. Jansen (eds), Making Globalization Sustainable, International Labour Organization and World Trade Organisation.

[15] See Cœuré, B. (2017), “Sustainable Globalisation: Lessons from Europe”, speech at the special public event “25 Years after Maastricht: The Future of Money and Finance in Europe”, Maastricht, 16 February 2017.

[16] See, for example, Eurobarometer Spring 2017.

[17] For a more extensive discussion of this point see Rodrik, D. (2017), “It is Time to Think for Yourself on Free Trade”, Foreign Policy, 27 January.

[18] See, for example, the ongoing debate on the Posted Workers Directive.

[19] European Commission (2016), “Communication from the Commission to the European Parliament and the Council – Anti Tax Avoidance Package: Next Steps towards delivering effective taxation and greater tax transparency in the EU”, Commission Staff Working Document, COM(2016) 23 final.

[20] 74% of EU citizens believe the EU should take more action in the field of fighting tax fraud. See Eurobarometer Spring 2017.

[21] See Wang, C., K. Caminada and K. Goudswaard (2014), “Income redistribution in 20 countries over time”, International Journal of Social Welfare, Vol. 23, Issue 3.

[22] See Draghi, M. (2017), “The interaction between monetary policy and financial stability in the euro area”, speech at the First Conference on Financial Stability organised by the Banco de España and Centro de Estudios Monetarios y Financieros, Madrid, 24 May.

[23] IMF (2017), “Are Countries Losing Control of Domestic Financial Conditions?”, Global Financial Stability Report, Chapter 3, April.

Source: ECB statement

Taguri: online banking BT Direct European Central Bank (ECB) Banca Centrala Europeana (BCE)

Comentarii

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

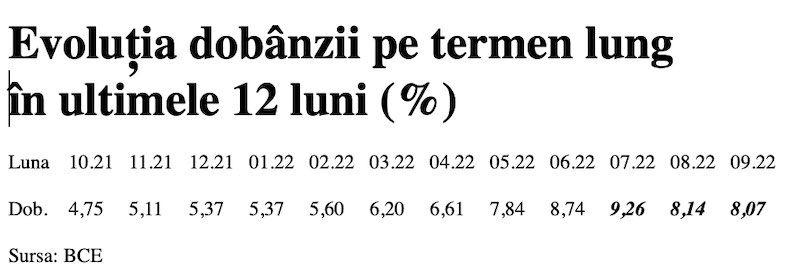

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

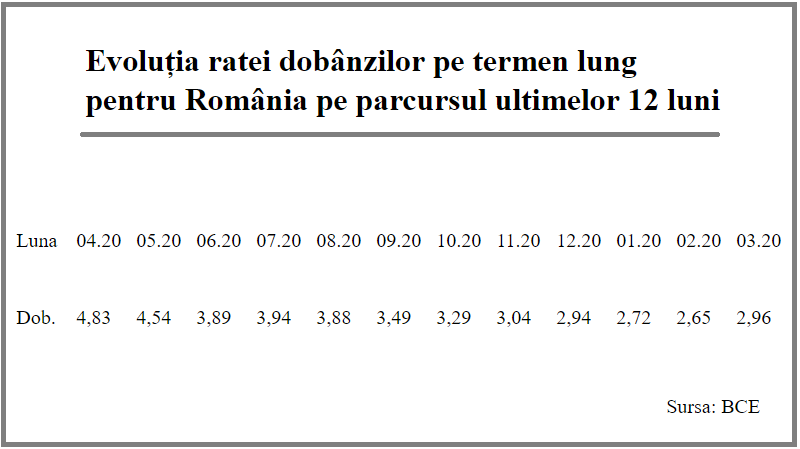

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent, aproape 20 miliarde euro după primele nouă luni

- Deficitul contului curent, aproape 18 miliarde euro după primele opt luni

- Deficitul contului curent, peste 9 miliarde euro pe primele cinci luni

- Deficitul contului curent, 6,6 miliarde euro după prima treime a anului

- Deficitul contului curent pe T1, aproape 4 miliarde euro

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Cate reclamatii primeste Intesa Sanpaolo Bank si cum le gestioneaza

- Platile instant, posibile la 13 banci

- Aplicatia CEC app va functiona doar pe telefoane cu Android minim 8 sau iOS minim 12

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

Analize economice

- România, „lanterna roșie” a cheltuielilor pentru cercetare-dezvoltare în UE

- Deficitul contului curent, peste 24 miliarde euro după primele zece luni

- Deficit comercial record în octombrie 2024

- Productivitatea în comerț, peste cea din industrie

- -6,2% din PIB, deficit bugetar după zece luni

Ministerul Finantelor

- Datoria publică, 51,4% din PIB la mijlocul anului

- Deficit bugetar de 3,6% din PIB după prima jumătate a anului

- Deficit bugetar de 3,4% din PIB după primele cinci luni ale anului

- Deficit bugetar îngrijorător după prima treime a anului

- Deficitul bugetar, -2,06% din PIB pe primul trimestru al anului

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- ANPC pierde un proces cu Intesa si ARB privind modul de calcul al ratelor la credite

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

Stiri economice

- Inflația anuală a crescut la 5,11%, prin efect de bază

- Datoria publică, 54,4% din PIB la finele lunii septembrie 2024

- România, tot prima dar în trendul UE la inflația anuală

- Datoria publică, 52,7% din PIB la finele lunii august 2024

- -5,44% din PIB, deficit bugetar înaintea ultimului trimestru din 2024

Statistici

- România, pe locul trei în UE la creșterea costului muncii în T2 2024

- Cheltuielile cu pensiile - România, pe locul 19 în UE ca pondere în PIB

- Dobanda din Cehia a crescut cu 7 puncte intr-un singur an

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- Sistemul bancar romanesc este deosebit de bine pregatit pentru orice fel de socuri

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Comerțul cu amănuntul - în creștere cu 8% pe primele 10 luni

- Deficitul balanței comerciale la 9 luni, cu 15% mai mare față de aceeași perioadă a anului trecut

- Producția industrială, în scădere semnificativă

- Pensia reală, în creștere cu 8,7% pe luna august 2024

- Avansul PIB pe T1 2024, majorat la +0,5%

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

împrumut

Vreau să apreciez pe Karin Sabine un împrumut de 9000€ pentru mine. Dacă aveți nevoie de un ... detalii

-

împrumut

Vreau să apreciez pe Karin Sabine un împrumut de 9000€ pentru mine. Dacă aveți nevoie de un ... detalii

-

Buna ziua! Am nevoie de ajutor!

Buna ziua! Am trimis activare cont si imi scrie ca au expediat QR Cod pe posta dar nu mia venit ... detalii

-

Înșelătorie

Mare atenție la firma vex group, te pune să investești 250 € în Forex, câștigi ceva și ... detalii

-

interdictie conturi ING

Buna ziua, o situatie ca cele de mai sus am patit si eu, cu diferenta ca Revolut a deblocat contul ... detalii