SEPA Instant Credit Transfer scheme is operational

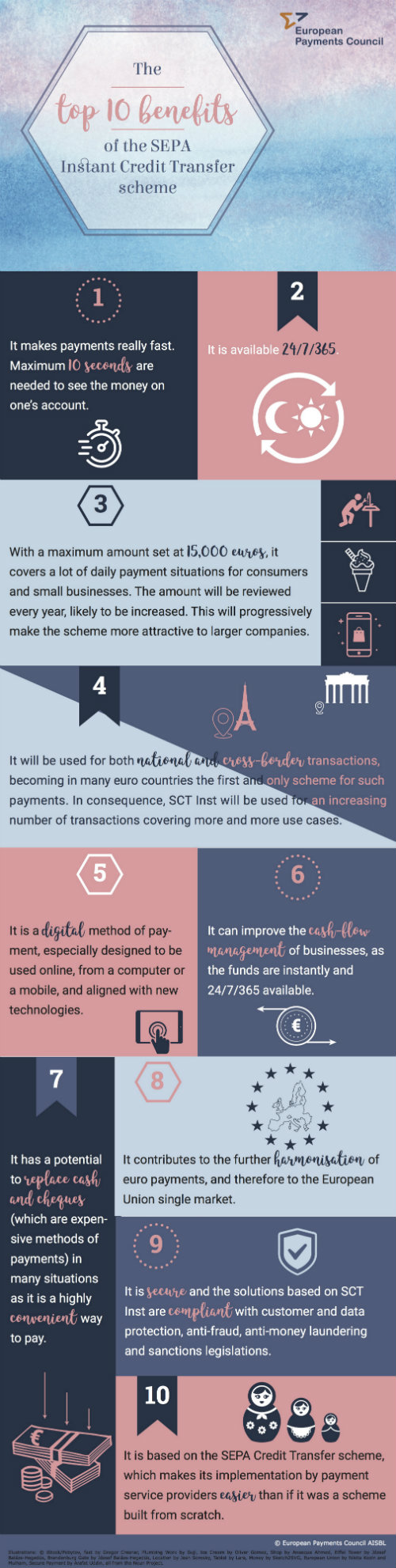

The SEPA Instant Credit Transfer (SCT Inst) scheme created by the European Payments Council is operational.

As of today, nearly 600 payment service providers (PSPs) from eight European countries are offering instant payment solutions based on SCT Inst.

Transferring money in less than ten seconds

The scheme allows the electronic transfer of money – currently up to 15,000 euros – progressively across Europe in less than ten seconds, at any time and on any day of the year, including weekends and holidays. The transactions covered by the scheme must be denominated in euros.

Nearly 15 percent of European PSPs already offer services based on SCT Inst

The 585 PSPs participating in the SCT Inst scheme are located in eight European countries: Austria, Estonia, Germany, Italy, Latvia, Lithuania, the Netherlands and Spain. Customers from these PSPs – individuals, businesses, corporations and administrations – can now make and receive instant euro credit transfers within their national borders as well as cross-border (starting with these eight countries), with the funds being immediately available.

SCT Inst is an excellent substitute to cash and cheques

SCT Inst offers an endless list of convenient uses for all segments of customers. It is especially highly convenient, for example, if an individual needs to urgently send money to a relative, or to pay for a product or service that requires on-the-spot settlement. With regular credit transfers, it can take up to one business day for the beneficiary to see the money in their account.

What is next for SCT Inst?

This is only the beginning of the European journey towards instant payments. The geographical scope of SCT Inst will progressively span over 34 European countries. More PSPs from major European countries are expected to join the scheme in 2018 and 2019.

Among them, PSPs from Belgium, Finland, Germany, Malta, the Netherlands, Portugal and Sweden.

What is more, the EPC will make the scheme evolve to better reflect market needs. This will be done in close dialogue with all payment stakeholders.

For example, the maximum amount per transaction will be regularly reviewed starting from November 2018. An increased maximum amount will make the scheme more attractive for companies.

With its numerous advantages, the SCT Inst scheme fully anchors European payments in the anywhere, anytime digital world.

Source: EPC statement

Comentarii

Nu există comentarii pentru această știre.

Adauga un comentariu

Alte stiri din categoria: ENGLISH

Neutral interest rate in Romania

The neutral nominal rate in Romania has been falling since the start of inflation targeting in 2005. The Taylor Rule clearly shows that interest rates peaked in 2022 and have been on a clear downward path ever since.Furthermore, the model estimates a long-term neutral nominal rate of around 3.9%, which is the equivalent of approx. 1.4% real.Using a more sophisticated model (i.e. New York FED’S HLW model), the real neutral interest rate in Romania is estimated currently at around 1.5% (1.7% 2023 average) and the historical mean at 1.2%.This implies a neutral nominal rate between 4.00% and 4.50%. In the past decade, the NBR real effective rate was below the neutral rate and only over the past year climbed above the neutral mark.Source: Erste Bank

Merger of Alpha Bank and UniCredit Bank Romania

Press Release:"Alpha Services and Holdings announces a strategic partnership with UniCredit in RomaniaMerger of Alpha Bank Romania and UniCredit Bank Romania and creation of third largest bank in Romania by... detalii

National Bank of Romania (NBR) Board decisions on monetary policy

NBR Board decisions on monetary policyIn its meeting of 4 April 2023, the Board of the National Bank of Romania decided:• to keep the monetary policy rate at 7.00 percent per annum;• to leave unchanged the lending (Lombard) facility rate at 8.00 percent per annum and the deposit facility rate at 6.00 percent per annum;• to keep the existing levels of minimum reserve requirement ratios on both leu- and foreign currency-denominated liabilities of credit institutions.The annual inflation rate went down to 15.52 percent in February 2023, from 16.37 percent in December 2022, relatively in line with forecasts. The decrease was mainly driven by the sizeable drop in the dynamics of fuel and electricity prices, under the impact of significant base effects and the change made to the energy price capping and compensation scheme starting 1... detalii

ING posts 2022 net result of €3,674 million, dividend of €0.389 per share

ING press release:ING posts FY2022 net result of €3,674 million,proposed final 2022 dividend of €0.389 per share 4Q2022 profit before tax of €1,711 million; CET1 ratio remains strong at 14.5%•Profit before tax up 29% on 4Q2021 and 24% on 3Q2022, mainly driven by higher income•Higher net interest income, as a further increase in liability margins helped offset TLTRO impact this quarter•Risk costs declined to 17 bps of average customer lending Full-year 2022 net result of €3,674 million, supported by growing customer base and increase in lending and deposits•On a full-year basis, our primary customer base grew by 585,000•Net core lending growth of €18 billion and net core deposits growth of €25 billion in 2022•Net result of €3,674 million in a challenging year; proposed final 2022 dividend of €0.389 per share CEO statement“Looking back, 2022 was... detalii

BT Financial Results as at 30 September 2022

BT Financial Results as at 30 September 2022

- No progress for the time being in Revolut becoming a subsidiary bank

- Risks may arise with some cross-border electronic invoice and card services

- ING posts 2Q 2022 net result of €1,178 million, supported by increased income and modest risk costs

- Sale of Raiffeisenbank (Bulgaria) EAD to KBC Bank closed

- Willi Cernko appointed new CEO of Erste Group

- Erste Group CEO Bernd Spalt decides not to renew contract

- First Bank launches the new cards collection

- NBR Board decisions on monetary policy

- Reflections on 20 years of the euro: joint article by Eurogroup members

Vezi toate stirile

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent, creștere cu 16% în ianuarie 2025

- Deficitul contului curent, aproape 30 miliarde euro în 2024

- Deficitul contului curent, aproape 20 miliarde euro după primele nouă luni

- Deficitul contului curent, aproape 18 miliarde euro după primele opt luni

- Deficitul contului curent, peste 9 miliarde euro pe primele cinci luni

Legislatie

- Decizia nr.105/2007 privind raportarea la Biroul de Credit

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

Lege plafonare dobanzi credite

- Care este dobanda maxima la un credit IFN?

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

Anunturi banci

- BCR este inchisa vineri, 18 aprilie, si luni, 21 aprilie

- Cererile de transfer de bani prin Whatsapp, Telegram, Messenger sunt fraude

- Un telefon sau mesaj care pare de la banca poate fi frauda

- Cererea unui ajutor in bani poate fi o inselaciune

- Cate reclamatii primeste Intesa Sanpaolo Bank si cum le gestioneaza

Analize economice

- Inflația anuală, redusă la 4,86%

- Comerțul, a cincea lună consecutivă de ajustare a creșterii

- Pensia reală a crescut cu peste 15% anul trecut

- Deficitul bugetar, rezultat slab după primele două luni

- Deficit comercial în creștere cu 38,5% pe ianuarie 2025

Ministerul Finantelor

- Deficitul bugetar, din ce în ce mai mare la început de an

- -8,65% din PIB, deficit bugetar pe anul 2024

- Datoria publică, 51,4% din PIB la mijlocul anului

- Deficit bugetar de 3,6% din PIB după prima jumătate a anului

- Deficit bugetar de 3,4% din PIB după primele cinci luni ale anului

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- ANPC pierde un proces cu Intesa si ARB privind modul de calcul al ratelor la credite

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

Stiri economice

- Deficitul comercial pe primele două luni ale anului, majorat cu 35%

- România, campioana europeană la șomajul tinerilor

- România, pe locul trei în UE la creșterea costului salarial în T4 2024

- Producția industrială, scădere conjuncturală în ianuarie 2025

- Datoria publică, 54,6% din PIB la finele lui 2024

Statistici

- România, marginal peste Estonia la inflația anuală

- România, a doua țară din UE ca pondere a salariaților cu venituri mici

- România, pe locul trei în UE la creșterea costului muncii în T2 2024

- Cheltuielile cu pensiile - România, pe locul 19 în UE ca pondere în PIB

- Dobanda din Cehia a crescut cu 7 puncte intr-un singur an

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Dobanda la euro scade la 2,25%

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- Sistemul bancar romanesc este deosebit de bine pregatit pentru orice fel de socuri

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- România, la 78% din PIB-ul mediu pe locuitor al UE

- Producția industrială, la cota -1,8% după 11 luni din 2024

- Deficitul contului curent, peste 26 miliarde euro în noiembrie 2024

- Comerțul cu amănuntul - în creștere cu 8% pe primele 10 luni

- Deficitul balanței comerciale la 9 luni, cu 15% mai mare față de aceeași perioadă a anului trecut

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate